The reported NAV — and the plan to rebuild it.

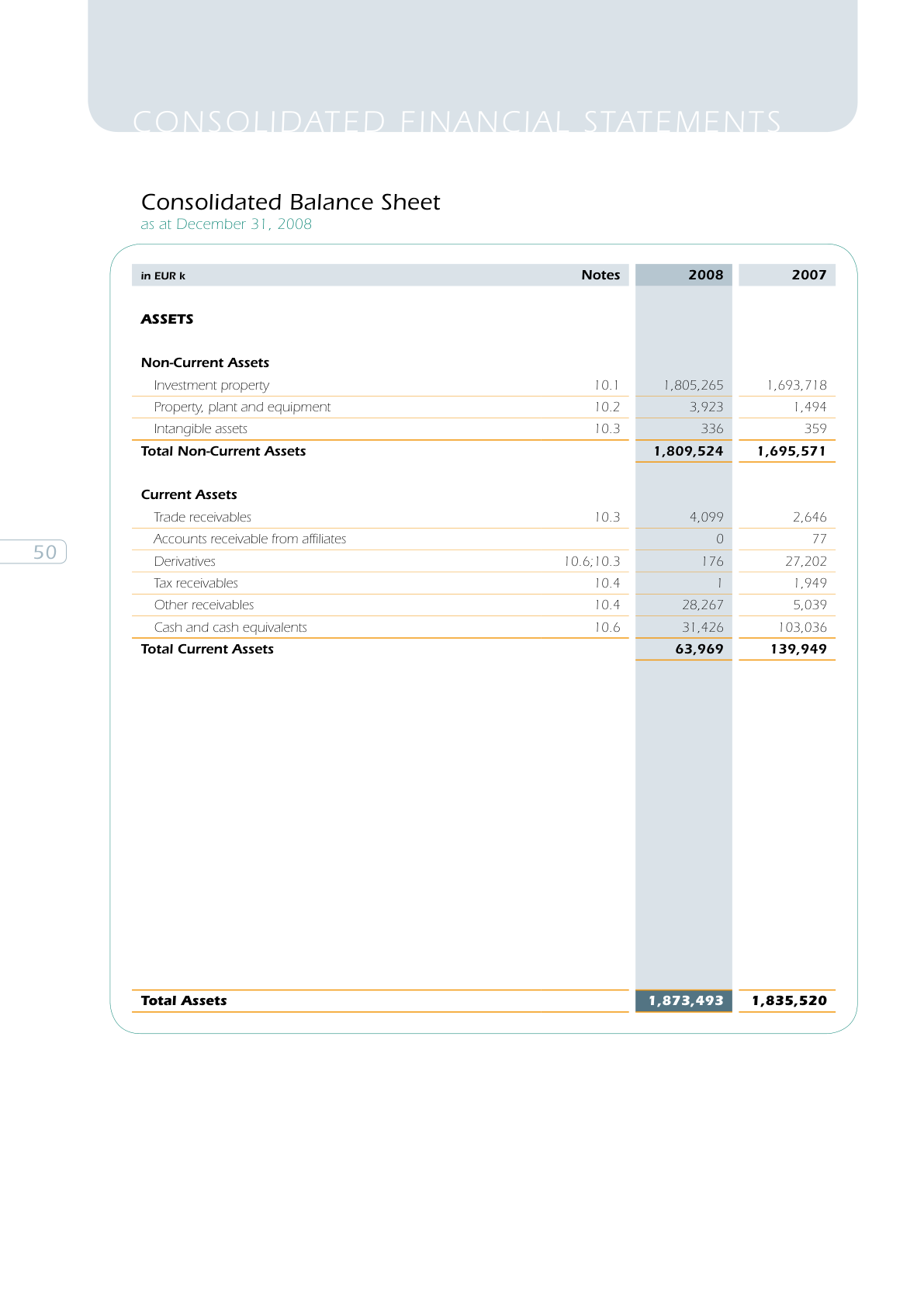

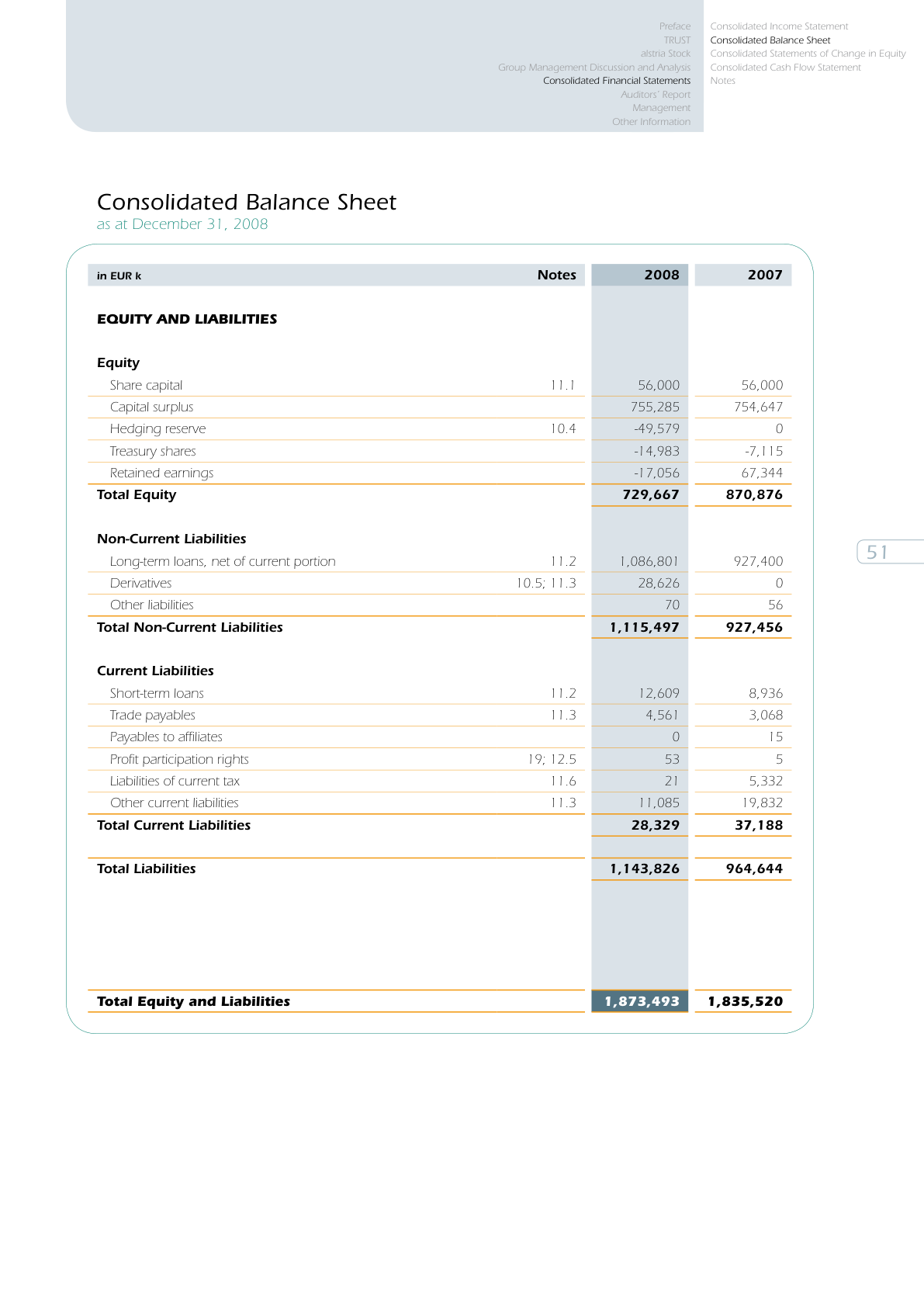

Alstria Office REIT, FY2008. The audited balance sheet, reshaped into the NAV calculation — and exactly which lines you'll independently re-value to land your own number.

Germany's first listed office REIT, year two, mid-crisis.

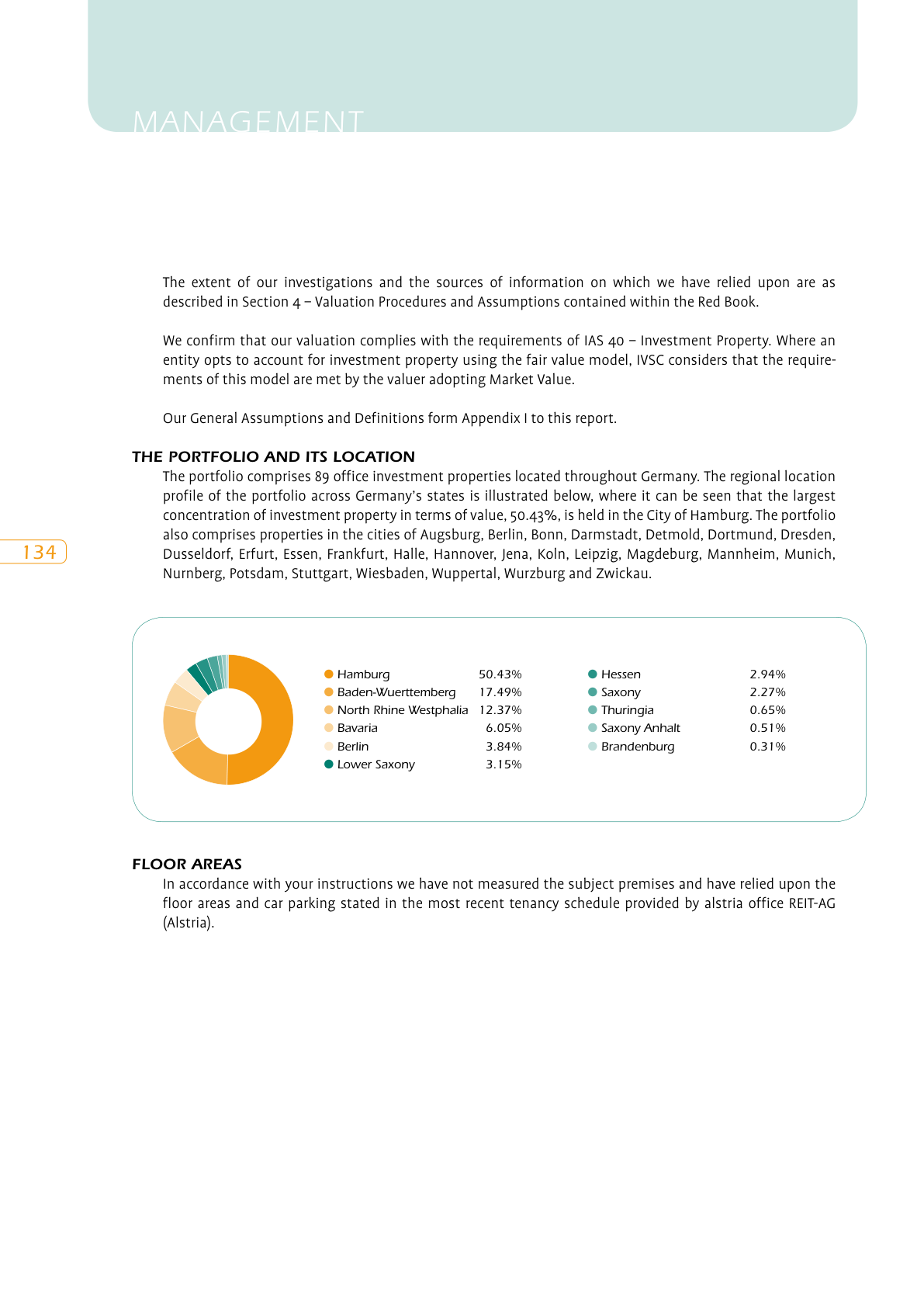

Alstria Office REIT-AG floated in April 2007 — Germany's first G-REIT — with a German office portfolio concentrated in Hamburg and Stuttgart. By early 2009, shares had fallen ~74% from their 2008 high and traded at a 73% discount to NAV, while the analyst community focused on financial-distress scenarios and deleveraging.

That reported NNNAV rests on property values set by an independent external appraiser — not the company's own marks. But an appraisal lags the live market. You'll build an independent NAV at current cap rates, from this annual report, to set against it.

Investment property at "fair value"

The portfolio sits at €1,805m (a 5.9% gross valuation yield) at 31 Dec 2008 — but valued on an income approach, for want of recent transactions. By the 31 March 2009 results date, the market had moved well past that mark.

Where the gap comes from

The cap rate re-values the property — almost all of the gap comes from there. The development & JV pipeline is the next-biggest difference from the appraised book. The debt barely moves it: it's floating-rate, so its carrying value already ≈ market.

From the balance sheet to a defensible NAV — in seven moves.

Each sub-module shows you a source document, asks for your judgment, then checks it against the analyst model. The output of one becomes the locked input to the next, so by SM5 the NAV bridge writes itself. SM6 reconciles your number to the reported NNNAV and itemises every delta.

Everything in this case traces to a real document.

The audited Alstria filings, the current market-yield evidence a March-2009 analyst would mark to, and the working model that shows how the calculation is structured. Every figure you'll validate traces back to a real document.